The business model is the ceiling

When the business model is the constraint, execution discipline raises the ceiling without breaking it. A diagnostic for model constraints.

Effort raises a structural ceiling. It doesn't break it.

One question tests for a business model constraint: does adding capacity require the resource that's already saturated? When yes, the model is the ceiling. In a custom delivery business, that resource is senior attention, and hiring consumes it. Working harder reproduces the ceiling at a different scale of effort.

The shape of the trap is a closed loop. Hiring requires revenue. Revenue requires capacity. Capacity requires hiring. Without external capital, the only resource that can grow capacity past the linear limit is the one already at saturation. Every execution improvement runs through that resource. The ceiling rises with the improvement. It still binds.

Why proportional cost growth caps revenue growth

Linear conversion keeps the constraint alive even after productivity improves. One more unit of revenue still requires one more unit of input from the bound resource. Code reuse, automation, and tooling discipline raise productivity. They don't change the linearity.

Custom work for individual clients is the clearest example. Each client requires requirements analysis, architecture, development, deployment, and support. Reuse covers some of it. The unrecoverable parts scale with client count. The ceiling is whoever has to do that work: founder capacity in a solo-operator service business, senior delivery capacity in a small flat-hierarchy team.

A productivity gain that lets four clients run on three engineers' worth of effort raises the ceiling. At 8 clients, capacity binds. At 16, again. The ceiling rises with each gain. It still binds.

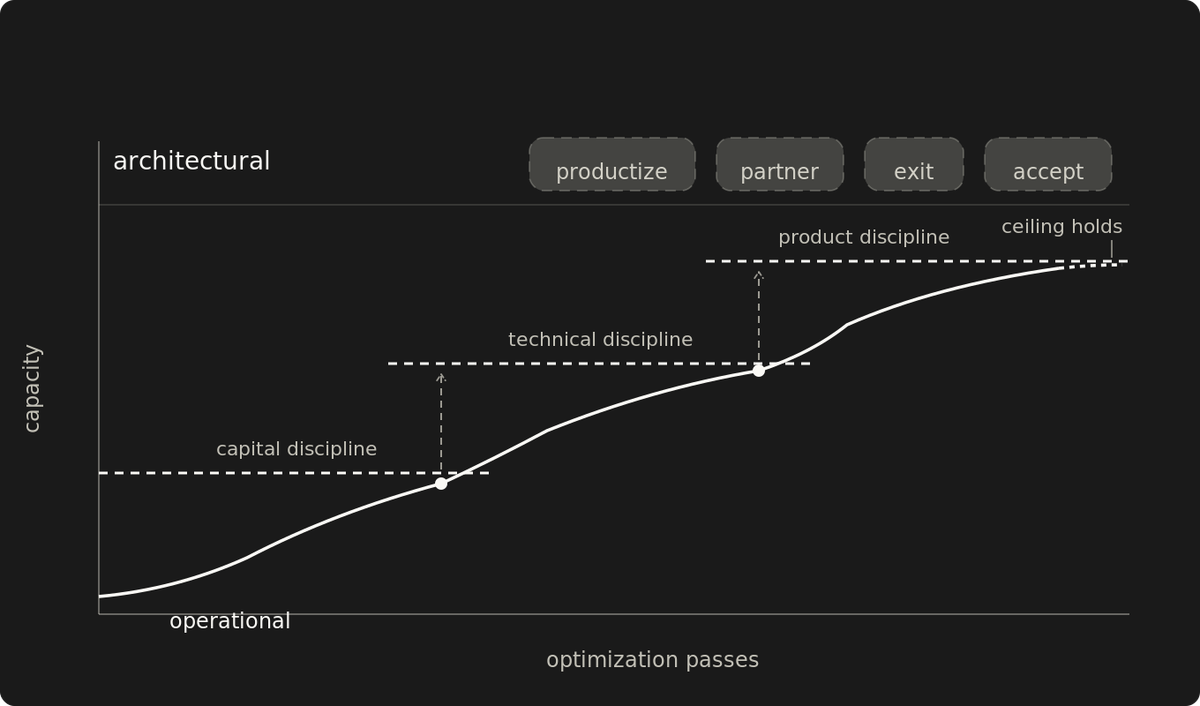

The lock survives execution discipline

Fifteen production systems ran under this lock. Three forms of execution discipline applied across the operation. The ceiling rose with each gain. It held.

Capital discipline: No outside investment beyond starting capital. No debt. Cash was not the only input. Prepayments and milestone billing could have funded a hire. The hire would still consume months of operator attention before producing net capacity. The loop stayed closed for the duration.

Technical discipline: 70-80% code reuse across the portfolio through a hybrid model: proven architectures repackaged per client. The model raised the productivity of the bound resource. It didn't change which resource was bound.

Product discipline: a multi-tenant SaaS platform on top of the existing codebase. Six modules. 95% code reuse from proven systems. Building, marketing, iterating, and supporting all required time pulled from client delivery. Productization needed attention before it produced leverage. It competed with delivery for the same scarce input. Productization only breaks the lock once the product runs without the producer. During the build it consumes the bound resource like anything else, and this one never crossed into that phase.

Capital, technical, product. The lock survived all three. Execution discipline scales the ceiling. Breaking it requires changing the model.

The exits are architectural

Four moves go beyond working harder. Each answers the same question: does this change how capacity is created? External capital can front-load capacity, but it doesn't change linear unit economics. Capital can fund the architectural exits, Productize and Partner. Capital alone, applied to a bound model, raises the ceiling without breaking it.

Productize. Detach delivery from the bound resource. Move from selling capacity (hours, headcount, attention) to selling instances of a product that runs without the producer once it's built. Cost grows slower than revenue on delivery and support, and the bound resource doesn't scale with each new sale. Acquisition is the exception: it can still climb as cheap channels exhaust, which is why productizing trades a delivery ceiling for a go-to-market one. Relabeling custom development as a "product" still scales with input.

Partner. Externalize capacity. The partnership only changes the ceiling when delivery and support ownership moves with it. Lead-generation alone shifts acquisition without relieving the bound resource. Only the partnerships that move delivery and support ownership relieve the bound resource: white-label, some reseller deals. Marketplace and integration that move only acquisition behave like lead-gen, shifting demand without relieving the bind. The model still scales with input, but the input is no longer the team's. The hard part moves into the relationship: who owns delivery, who owns the customer, who owns the support load.

Exit. Move the skill into a model with existing capacity: an employer, an acquirer, or a platform with built-out distribution. The ceiling moves because the model changes. The skills survive the transition. The bound resource type changes with the model.

Accept. Optimize inside the known bound. Acceptance is a coherent strategic choice when the lifestyle and margin profile of the bound model is the goal. It stops being coherent when the operator confuses it with execution: running optimization passes against a structural ceiling, reading the absence of breakthrough as a discipline problem.

Three of the exits restructure how the model converts inputs to outputs. Accept keeps the conversion as it is, architectural in altitude but operational in content. Optimization passes are operational. They squeeze the existing conversion. When optimization stands in for architecture, the result is years of effort that scale the ceiling without breaking it.

The diagnostic

The diagnostic is binary. Does adding capacity require the resource that's already at saturation? If no, this capacity loop isn't what's binding, and the constraint is elsewhere: distribution, demand, addressable market. If yes, the model is the ceiling.

When adding capacity requires the bound resource itself, the next decision is architectural, not operational.